The discovery of Pegasus‑1 in the Eastern Mediterranean is being hailed as a turning point not only for Turkey’s energy outlook but for regional energy logistics altogether. While the exploration itself is a major technical and strategic success, it opens up a far more complex question: how will the gas actually get to market?

Natural gas fields, no matter how large or promising, are only as valuable as the infrastructure that supports their extraction, transportation, and delivery. Pegasus‑1 sits in a region where pipelines intersect with politics, and where every cubic meter of gas is also a unit of geopolitical leverage. That makes its future pathway just as crucial as its volume or pressure.

Infrastructure Meets Geopolitics

The Eastern Mediterranean is home to more than underwater reservoirs. It’s a dense and volatile theatre of maritime claims, national interests, and overlapping energy corridors. Turkey’s energy strategy is increasingly driven by two simultaneous goals: becoming a self-sufficient energy producer and reinforcing its role as a regional energy hub.

Pegasus‑1 checks both boxes—but only if the gas can be delivered. To do so, Turkey and its energy partners are weighing three primary options: connecting to existing pipelines such as TANAP, investing in LNG infrastructure, or building a dedicated offshore export route.

Each path has implications far beyond engineering, touching on diplomacy, climate strategy, investment risk, and long-term energy security.

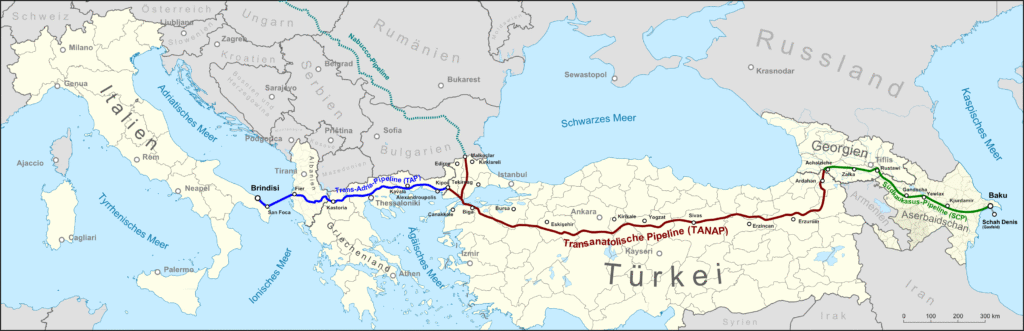

Option One: Tapping into TANAP

The Trans-Anatolian Natural Gas Pipeline (TANAP) was designed to carry Azerbaijani gas to Europe, passing through Turkish territory before joining the Trans Adriatic Pipeline (TAP). With Turkey already maintaining and expanding its domestic grid, Pegasus-1 gas could potentially be connected to this infrastructure with limited construction compared to an entirely new corridor.

This scenario is attractive because it is both cost-effective and already partially sanctioned by European interests. The Southern Gas Corridor is seen by Brussels as a key mechanism for reducing dependence on Russian imports. If Turkish gas from Pegasus‑1 can join that flow, it might gain political as well as economic favor.

However, capacity is finite. TANAP was built with specific throughput in mind, and expanding it to accommodate new gas may require complex negotiations with Azerbaijan and the EU. Furthermore, EU energy policy is increasingly defined by decarbonization targets. How willing Europe is to support another fossil fuel pipeline—regardless of origin—remains a subject of debate.

LNG: Flexibility with a Price

Turkey already operates several LNG terminals and floating storage regasification units (FSRUs), giving it the foundation to consider a liquefied export strategy for Pegasus‑1 gas. This would offer flexibility in reaching global markets, including Asia and Latin America, which cannot be accessed by pipeline.

Yet the challenges are considerable. Liquefaction facilities require years to build and billions of dollars in investment. They also introduce an added layer of complexity, as gas must be cooled to -162°C, shipped, and then regasified at the destination. Environmental regulations are also becoming stricter, with LNG operations facing scrutiny over methane leakage and lifecycle emissions.

Despite that, LNG might be one of the few paths available if geopolitical conditions limit pipeline cooperation or market demand shifts toward short-term, floating supply agreements.

The Offshore Pipeline Option

The third scenario under discussion involves a purpose-built pipeline that could run from the Pegasus‑1 site through the Mediterranean toward either Greece or Italy. Though ambitious, such a project could emulate, at least conceptually, the once-proposed EastMed Pipeline—now largely shelved.

An offshore route could bypass territorial disputes on land and reduce dependency on third-party transit states. However, the costs of undersea construction—particularly in deep waters—are prohibitively high. Add to that the security vulnerabilities exposed by incidents like the Nord Stream sabotage, and offshore pipelines begin to look less like strategic solutions and more like strategic risks.

Unless a consortium of state and private stakeholders steps in to distribute risk and cost, this option remains the most politically independent but economically uncertain.

Commercialization Will Require Cooperation

Regardless of the transportation route selected, Pegasus‑1’s gas will not flow without cross-border and cross-sector cooperation. Turkey may be the operator and sovereign actor, but such projects depend on financing, technology partners, and off-take agreements that cross multiple jurisdictions.

At the moment, potential partners include pipeline stakeholders like SOCAR and TAP consortium members, global LNG buyers, and possibly multilateral lenders such as the European Investment Bank or the Asian Infrastructure Investment Bank.

Private investment will likely be influenced by the perceived legal and political stability of the project, the clarity of Turkey’s regulatory framework, and the market’s long-term confidence in gas as a transition fuel.

Global Market Timing

Timing is everything. While energy security remains a top priority for many nations—particularly following the disruptions in 2022—most Western countries are also accelerating their transition toward renewables.

This dual-track pressure means that Pegasus‑1 must move quickly to capture current demand windows. Infrastructure decisions made now will shape its commercial relevance for the next 25 to 30 years.

European gas demand is expected to decline gradually after 2030, but in the interim, the EU still needs reliable, politically stable sources to replace lost volumes from Russia and meet winter peaks. Whether Pegasus‑1 can be part of that mix depends on how soon it comes online, how competitively it’s priced, and how politically aligned it is with the broader climate agenda.

A New Test for Regional Energy Diplomacy

Pegasus‑1 is more than a resource; it’s a test case. It reflects Turkey’s ability to balance domestic energy ambitions with its role in international supply chains. The route this gas takes will signal how Ankara views its energy diplomacy—whether it prefers regional integration, global flexibility, or sovereign infrastructure development.

At the same time, European actors will be watching to see if this new supply source can be integrated into the continent’s energy mix without complicating existing balances or undermining the green transition narrative.

In many ways, Pegasus‑1 is not only about energy—it’s about strategy, influence, and timing in an increasingly unstable global order.

Sources:

- International Energy Agency (IEA), Natural Gas Market Reports: https://www.iea.org

- Atlantic Council, Turkey’s Energy Strategy in the 2020s, 2024

- European Council on Foreign Relations, Pipeline Politics in the Eastern Mediterranean, 2023

- BOTAŞ Official Infrastructure Maps and Reports: https://www.botas.gov.tr

- S&P Global Commodity Insights, Eastern Mediterranean Energy Update, Q1 2024